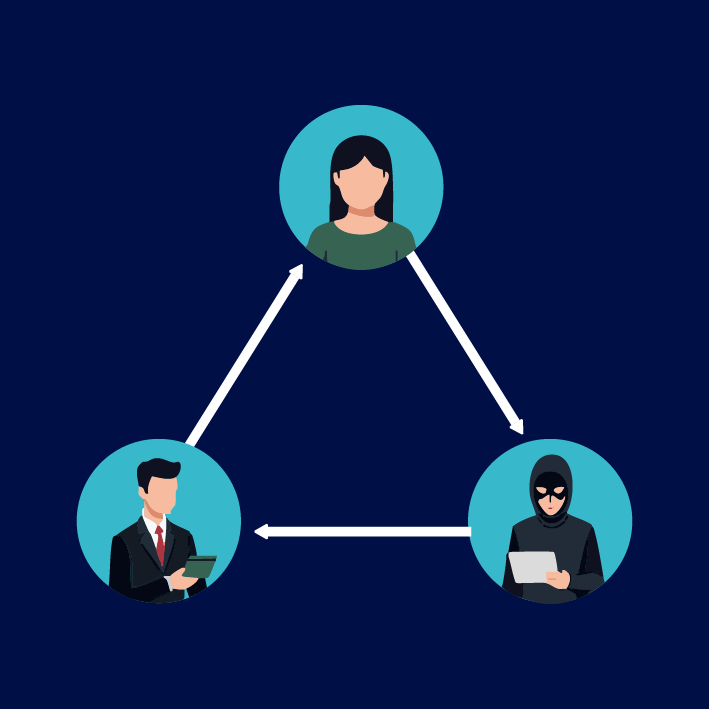

What is Triangulation Fraud? How to Defend Against Reseller Scams

Consider the perfect eCommerce sale. An honest customer buys a product online that the merchant fulfills. The merchant earns business revenue, while the customer receives a needed good or service. Everyone is happy.

Fighting Shopify False Declines With FUGU

Over the years, Shopify has earned its place at the top of the eCommerce food chain, with sellers in 175 countries in the world. Because of its popularity, fraudsters see businesses on Shopify as attractive targets.

Fighting Authorized Push Payment (APP) Fraud Post Payment

Payment scams are rampant. The Federal Trade Commission (FTC) shows that consumers filed a staggering 2.5 million fraud reports in 2023, amounting to more than $10 Billion in losses. Of those reports, 853935 were imposter scams, marking an increase from 2022. In addition, 80% of businesses reported attempts of fraud activity last year. Everyone is at risk.

Maximizing conversions with ecommmerce payment configuration

Finding the right way to maximise conversion while protecting your eCommerce store from fraud is crucial for growing your business.

When the cost of handling policy abuse cost more than managing your company’s grow

As online retail continues to flourish, the specter of policy abuse looms large, presenting a multifaceted challenge that eclipses traditional eCommerce fraud. In recent years, the surge in eCommerce revenues has been paralleled by a corresponding increase in fraudulent activities, as economic uncertainties compel consumers to test the boundaries of acceptable behavior, resulting in a myriad of policy abuses.

How Fraud Effects on Your Customer Lifetime Value

In the fast-paced realm of e-commerce, where competition is fierce and customer acquisition costs are on the rise, maintaining a high Customer Lifetime Value (LTV) is paramount for sustained success.

Fighting False Declines: How FUGU Stands Out

In the vast landscape of Commerce, merchants face a myriad of challenges, with false declines standing out as particularly detrimental. These erroneous rejections not only result in lost revenue but also harm customer relationships, leading to a ripple effect of negative consequences.

Understanding the True Cost of eCommerce Fraud

eCommerce fraud presents a dual challenge to merchants: direct financial losses from fraudulent transactions and the operational costs incurred in fighting fraud.

Maximizing Success in Chargeback Disputes

Chargebacks are a significant challenge in eCommerce, leading to financial losses and potential harm to a business’s standing with payment processors. Successfully navigating chargeback disputes requires a deep understanding of the process and a strategic approach to evidence collection and presentation. Here, we outline effective strategies for winning chargeback disputes, enhanced by the innovative capabilities of FUGU.

The Impact of Resellers Abuse

In the world of eCommerce, the phenomenon of third-party reselling has become a significant challenge. These resellers use sophisticated methods, including bots, to acquire products in large quantities and resell them at inflated prices.